NEW BUSINESS • 11 AUGUST 2021 • 9 MIN READ

How to start a business in Australia and get set for success

What entity type suits my business? How do I comply with tax law and legislation? How do I become an employer and who do I go to for help? Whether you’re an individual or entity looking to become an Australian tax resident, or you’re setting up a permanent business establishment, this guide will help you stay compliant and lay the foundation for long term success.

Which business entity type should I choose?

When entering business in Australia, the first step is to decide what type of entity you will use to undertaken your business The main entity types are:

Company

A company is a separate legal entity that provides limited liability to its shareholders. This makes it an ideal structure for high risk businesses but also businesses that are looking to grow and scale. This is the most common vehicle used when a foreign company begins trading in Australia.

A foreign company looking to carry on business in Australia is usually carried out by establishing a subsidiary (company that is owned and controlled by the foreign company) or registering a branch office. However, the Australian company can be set up with any shareholders that the foreign company desires.

As well as being required to abide by the rules of the Australian Tax Office (ATO), companies are also required to abide by legislation administered by the Australian Securities and Investment commission (ASIC).

One of these regulations is that an Australian company is required to have an Australian resident director.

Sole trader

A sole trader is a business that is being run under an individual’s name. It is the cheapest and easiest structure to establish and is often favoured by small contractors, tradies, home based businesses and online businesses.

In contrast to a company, there is no limit of liability to business assets. An individual will be personally liable for all debts incurred by them and claims made against them in carrying out their business.

Operating as a sole trader in Australia is very uncommon for a foreign resident, due to the unfavourable tax rates on foreign residents (See tax rate table below).

Trust

While most commonly used as an investment vehicle, a trust can also be used as a trading vehicle. When structured correctly a trust is able to offer limited liability for the trustee’s of the trust. While a trust has excellent income splitting capability, it is not a suitable vehicle for growing and scaling a business. A trust is often used when control and benefit is maintained within a family group.

In addition to the compliance with the ATO, trusts are also governed by trust specific legislation.

Partnership

A partnership is an association of two or more entities who carry on business in common. A partnership is relatively low cost to establish however, similar to a sole trader, the partners are jointly liable for the debts and actions of each of the other partners. Partnerships are commonly used in professional service businesses.

Comparison

How do I comply with Australian tax laws?

Once you have selected your entity type, you will need to ensure you are complying with all relevant regulations and understand what registrations apply to your business. While some registrations are mandatory for all businesses, others will be dependent on your operations and circumstances. Let’s take a look at the most common registrations.

Tax File Number (TFN)

Australian Business Number (ABN)

Business name registration

Goods and Services Tax (GST)

Pay As You Go Withholding (PAYGW)

Pay As You Go Instalments (PAYEGI)

Fringe Benefit Tax (FBT)

State taxes

Tax File Number (TFN)

A TFN is an entity’s personal identification number issued by the ATO.

All businesses need a TFN and all entities will have a single TFN. Eg. If you are a sole trader, your individual TFN is used for both your business and your personal affairs.

Once you register for a TFN you are required to lodge an annual income tax return. The standard tax year in Australia runs from 01 July to 30 June.

Australian Business Number (ABN)

An ABN is a business identifier that is unique to a business entity and it simplifies interaction with customers, other businesses and the government.

Registration is compulsory if your turnover is greater than $75,000. While it is not compulsory to have an ABN if your turnover is less than $75,000, it can be impractical not to, given business to business payment withholding rules (businesses must withhold 47% of the sale from a business with no ABN) and banking requirements. Additionally, you need to consider the public perception of not holding an ABN (customers may question your credibility).

An ABN is granted per entity and not per business enterprise. This means a single ABN holder may operate a retail store as well as a cleaning business under the same ABN.

Both an ABN and a TFN are managed by and applied for through the Australian Business Register (ABR). It is an online form that will require proof of identity of all associates of the business to be provided in hard copy to the ABR.

Business name registration

Companies, partnerships and trusts are required to register a business name. If you’re a sole trader and conduct business under a different name (“…trading as…”), you also need to register.

Your business name will be linked to the ABN of your entity.

Goods and Services Tax (GST)

GST in Australia is 10%. Registering for GST requires you to include GST in your sales (which gets paid to the ATO) and allows you to claim GST credits on eligible expenses.

As with an ABN, you are required to register for GST when your annual business turnover exceeds $75,000; registration is otherwise voluntary.

If you expect to incur significant startup costs or purchase large assets, it may be beneficial to voluntarily register for GST even if your turnover is less than $75,000. The GST credits may provide you with cash flow benefits for the business.

Once you have registered for GST you are required to lodge a Business Activity Statement (BAS). If your registration is voluntary, your BAS can be filed on an annual basis. If not, then this must be filed quarterly or monthly.

If you are an exporter to Australia, you may be required to register for Australian GST for low value imported goods, or importers services and digital products. There is a simplified registration process for this.

Pay As You Go Withholding (PAYGW)

You are required to register for PAYGW if you make payments that are subject to withholding, even if you do not withhold any amount. The most common reason to register for PAYG is when you are an employer.

Other payments subject to withholding are payments to directors, to businesses that don’t quote their ABN, along with dividends, interest and royalty payments made to non-residents of Australia.

Once registered for PAYGW you are required to report the withholding amounts in your BAS.

Pay As You Go Instalments (PAYGI)

PAYGI are regular payments made to the ATO that are credited to your tax bill for the tax year it is paid for (similar to making provisional tax payments in New Zealand). These payments assist in planning your cash flow to ensure you do not have a large tax bill when you lodge your tax return.

An entity will be placed on the PAYGI system where:

Individuals and Trusts

- Instalment income (income from business or investment) is $4,000 or more

- Tax payable in your latest return exceeds $1,000

Companies

- Instalment income exceeds $2 million

- Estimated annual tax of $500 or more

Once registered for PAYGI, you are required to make payments in your quarterly BAS.

Fringe Benefit Tax (FBT)

Employers who provide fringe benefits (non-cash benefits) to employees must register for FBT.

The most common fringe benefits provided to employees are the private use of business motor vehicles and providing entertainment.

Once registered, you are required to lodge an annual return and may be required to pay FBT instalments if your FBT bill for the last financial year was $3,000 or more. FBT is charged at 47% of the taxable value of the benefit.

State taxes

Australia also has various state-based taxes and laws that may impact your business. The most common is payroll tax.

Payroll tax is a state tax assessed on wages paid or payable to employees (and contractors deemed to be employees) whose total Australian taxable wages exceeds the threshold amount set by the state.

Registration is self assessed and you will be required to register once your monthly payroll exceeds the monthly threshold.

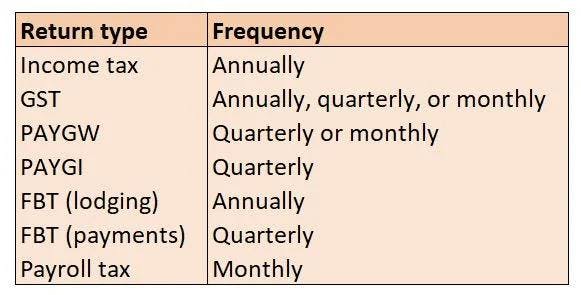

When to lodge or pay taxes

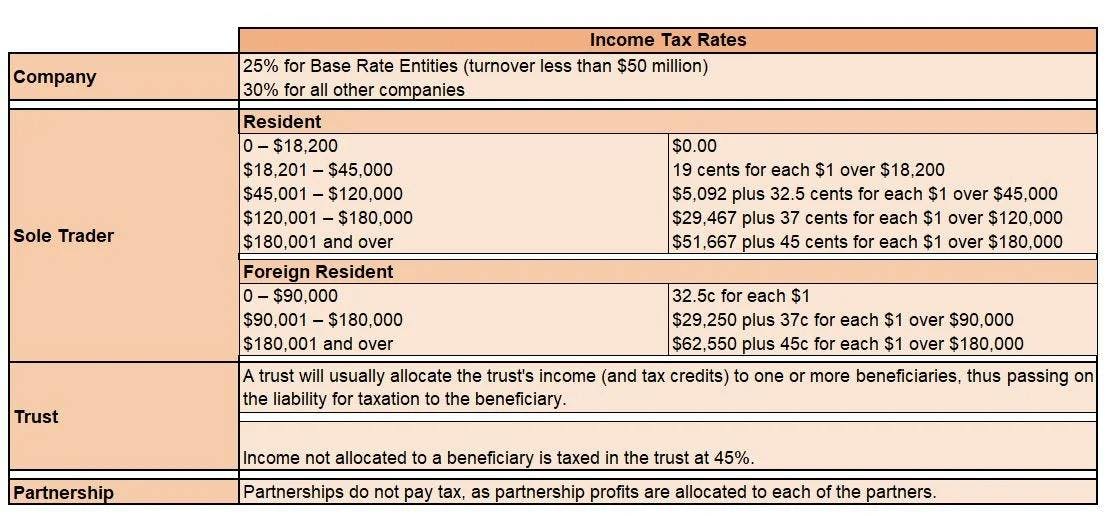

Income tax rates for Australian businesses

How do I employ people in Australia?

When employing individuals in Australia there are minimum requirements that all employers must meet in addition to the ATO’s registration and lodgement obligations. These are outlined below:

National Employment Standards (NES)

The NES has 11 minimum employment entitlements that have to be provided to all employees. These standards cover the following minimum requirements:

- Maximum weekly hours

- Requests for flexible working arrangements

- Offers/requests to move from casual to permanent

- Parental leave and related entitlements

- Annual leave

- Personal, carers, compassionate and unpaid family and domestic violence leave

- Community service leave

- Long service leave

- Public Holidays

- Notice of termination and redundancy

- Fair Work Information Statement and Casual Employment Information Statement

Superannuation

Superannuation is money that is set aside for the retirement of an individual. Employers are required to make “super guarantee” payments to an employee’s superannuation fund, when the employee earns more than $450.00 per month. The super guarantee amount is currently 10% of gross wages. This is similar to the New Zealand Kiwisaver scheme, except there is no requirement for the employee to make contributions, and it is compulsory (i.e. employees or employers can’t opt out).

Insurance

Workers compensation insurance provides protection for an employer in the event that one of their employees suffer a work related injury or illness.

All employers that pay more than $7,500 in annual wages are required to have workers compensation insurance.

Your accountant to the rescue

We understand. Trolling through rules and regulations constantly to keep yourself safe and legal takes you away from doing what you set out to do; run your business.

Our Beany accountants are experts at keeping you compliant, supporting you through your business journey, and understanding your goals whilst working with you to achieve them.

Create your free account or contact us today and one of our friendly Beanies will be in touch to discuss your goals and help where we can.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Julian Hutabarat

General Manager, Beany Australia

I started my accounting career in 2012 and obtained my CPA in 2015. Outside of work I enjoy mountain biking and hope one day to ride Crank It Up! at Whistler.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

Starting a business - have you thought about...?

February, 2022We know you have hundreds of thoughts and ideas when setting up your business and you’re bound to overlook some asp...

Business structures – what’s best for you?

October, 2021Sole trader, partnership, and company are the common business structures in Australia. Making the right decision re...