TAX • 7 OCTOBER 2021 • 10 MIN READ

Dividends and Imputation Credits

It’s always nice receiving dividends. You receive the money in your bank account and it’s already been taxed at source – just like interest from the bank. Ever thought about the other side – the company paying out the dividends? Or what would be needed for your own company to declare dividends?

Dividends is one way for a company to distribute profits to its owners (shareholders)*. Before a company can declare a dividend, the directors must be satisfied that a solvency test be met:

- the company will still be able to meet its debts as they come due, and

- assets are greater than liabilities (including contingent liabilities)

Another, more common method, is to allocate the profit as a shareholder salary.

Dividends

Dividends are income to the person receiving them. However, dividends come from company profits after tax has been paid. If the person receiving the dividend was required to pay full tax on the dividend income, it would be double taxation (the profit is taxed in the company, then the after-tax profits taxed again on dividend income to the shareholder).

Imputation Credits (ICs) mitigate a portion of this. An imputation credit is a credit for tax already paid by the company – it’s passed onto the shareholders and ‘attached’ to the dividend.

Dividends must be taxed at 33%. As the New Zealand company tax rate is 28%, the company needs to top-up tax paid to Inland Revenue. The extra 5% is paid by the company as Dividend Withholding Tax (DWT).

The dividend going out to the shareholders is now what we call ‘fully-imputed’. Although the dividend is taxable income to each shareholder, the shareholder can reduce the tax charge by including the ICs and DWT as tax credits.

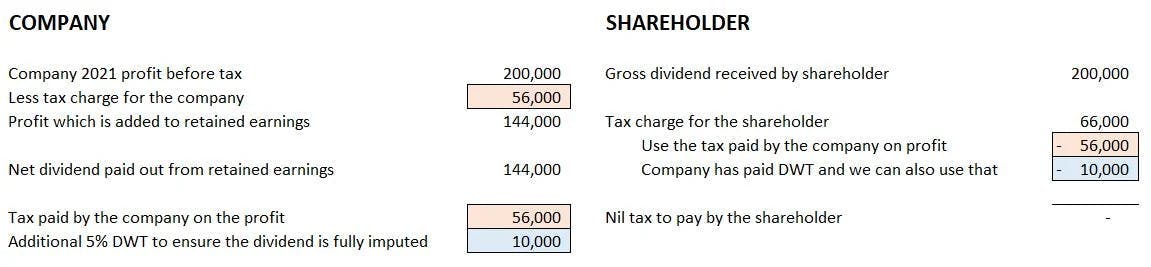

Below is a demonstration of how this would work in the most simplest of cases.

The company’s dividend statement will show the number of ICs and DWT – you don’t need to work it out yourself.

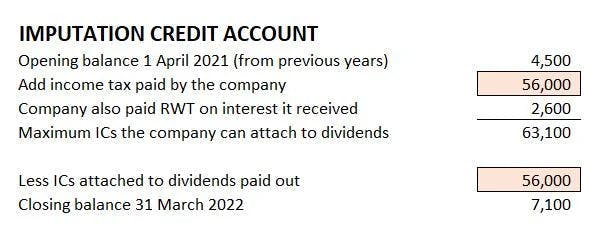

Imputation Credit Account

In order to keep track of the tax credits available to pass on, the company must maintain a notional account known as the Imputation Credit Account. This account records all the tax transactions – tax payments, tax refunds, ICs forfeited*, ICs attached to dividends paid.

Once a dividend has been issued, the balance in the imputation credit account held by the Company reduces by the amount of tax attached to the dividend.

Following on from the Dividends section above, here is an example of a simple ICA:

* The most common reason for ICs to be forfeited is where shareholders have changed during the year

Only companies

Because only companies use dividends to pass profits to their owners (shareholders), they are the only type of entity required to maintain an ICA. This does not extend to look-through companies, where all profits are passed directly to the owners without requiring a dividend.

At the end of the year, the company files a return with Inland Revenue which details what has happened in their ICA that year. Your accountant will collate and return this for you, and will also keep a record of all the transactions that have taken place in your Imputation Credit Account.

Imputation Credit Account with a debit balance at the end of the year

There are situations when the company can have a debit balance in the ICA. If this occurs as a closing balance, the company must pay an amount to Inland Revenue to clear the balance back to $0, plus a 10% penalty.

The main cause of the debit balance usually centres around dividends being paid or a loss of shareholder continuity, so it’s important that your accountant assists with calculating the amount and setting the timing of dividends.

Shareholder continuity

Similar to business losses, Inland Revenue believes that in order to benefit from the tax paid by a company, you need to be a shareholder when the tax is actually paid. In order not to lose (forfeit) any imputation credits, a company needs to have a minimum of 66% of the same shareholders from the date the tax was paid until the date they’re passed on to the shareholders.

If you’re thinking about changing any shareholdings in your business, talk to your accountant first so that you can maintain the best tax position possible.

Franking credits

A franking credit is the Australian equivalent of an imputation credit. Unfortunately, if you receive a dividend with franking credits attached, you’re unable to claim those as tax paid in your New Zealand tax return. Some Australian Companies pay New Zealand tax as well, and will attach this as Imputation Credits to your dividend – these you can claim.

As you can see, paying dividends is complex. Problems can easily develop if you get the timing and/or amounts wrong.

Beany can take the uncertainty out of the process by calculating the dividend, imputation credits, and dividend withholding tax. We also prepare the required legal documentation, such as director(s) resolution, insolvency certificate, the dividend statements sent to shareholders, and filing the dividend withholding tax return.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant would.

We have a dedicated team of remote accountants to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Jess Heslop

I'm an ex-big 4 CA and a technology enthusiast, based in Nelson where I live with my husband and two young children.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

What is withholding tax?

February, 2022Sometimes it can be a minefield trying to understand all the different kinds of taxes! Here we will look at the mai...

A guide to income tax for business owners

March, 2021Answering the most frequently asked questions about income tax and the basics business owners need to know about pr...

The basics business owners need to know about GST

March, 2021GST is a tax everyone pays on goods and services while living out their day-to-day lives. Businesses collect this ...